If you’ve ever moved to another European country, taken a freelance gig abroad, or tried to pay a bill in euros from a foreign bank account, you may have encountered a maze of unfamiliar acronyms. People talk about SEPA transfers as if everyone knows what they are, yet they rarely explain why a transfer within the euro area feels so different from an international wire.

You might search for the European equivalent of the United States’ Automated Clearing House and wonder whether SEPA transfers explained are just another term for regular bank transfers. At coffee shops in Berlin, you hear stories of friends being able to pay rent back home with no extra charge, while others complain about unexpected fees. This confusion is understandable; the Single Euro Payments Area (SEPA) is designed to make euro payments seamless across 41 countries, but its mechanisms remain obscure for many users. Let’s unpack how this system works and why it has been called Europe’s answer to ACH.

Table of Contents

SEPA: Europe’s Unified Payment Infrastructure

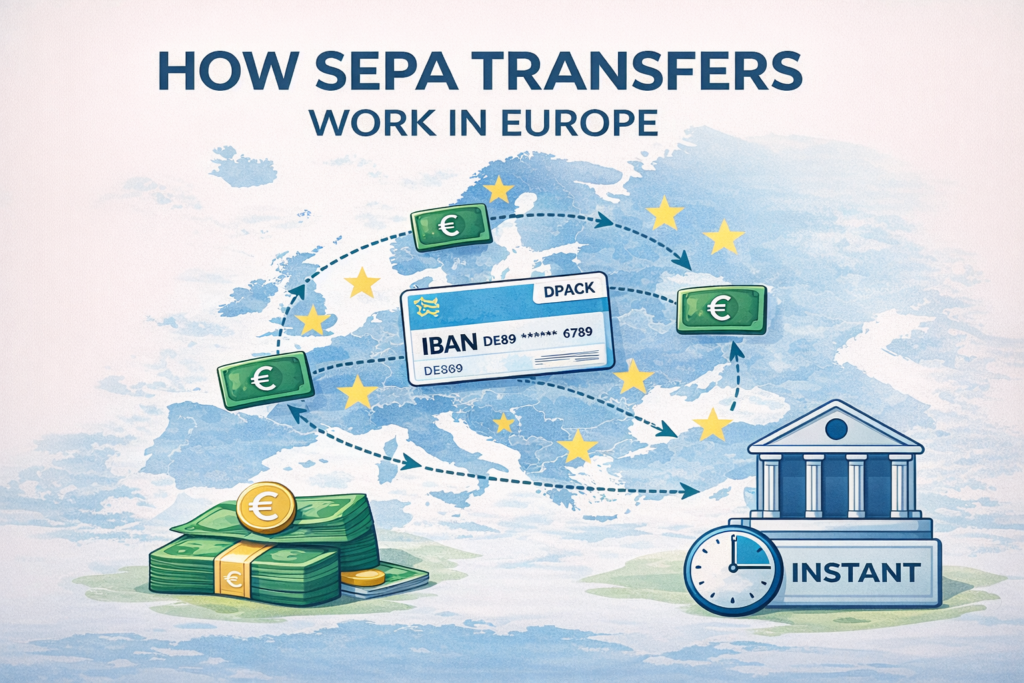

The Single Euro Payments Area is a framework that allows people and businesses to make cashless euro payments anywhere in the European Union and in several non‑EU countries “in a fast, safe and efficient way, just like within their own country”. Before SEPA, cross‑border euro payments were treated as international transfers, often accompanied by higher fees and slower processing. Harmonised standards across SEPA have eliminated differences between domestic and cross‑border payments, helping make the European economy more efficient and competitive. In that sense, SEPA functions as Europe’s version of ACH—an infrastructure enabling bank‑to‑bank transfers—but with a unique regional twist: it extends beyond national borders.

What Is SEPA? A Short History and Scope

SEPA was launched by the European banking and payments industry with support from national governments, the European Commission and the Eurosystem. It currently covers 41 countries, including all EU Member States and several non‑EU nations and territories. SEPA is not limited to eurozone members; countries like Sweden and Denmark participate even though they do not use the euro as their domestic currency. The goal of SEPA is to standardise the way non‑cash euro payments are conducted so that, whether you live in Madrid, Paris, Dublin or Warsaw, a euro transfer feels like a domestic transaction.

The core of SEPA is a set of payment schemes developed by the European Payments Council and administered through agreed technical standards. Three main instruments operate within SEPA:

- SEPA Credit Transfer (SCT). A payment initiated by the payer that moves money from their account to the payee’s account.

- SEPA Instant Credit Transfer (SCT Inst). A real‑time version of the credit transfer that makes funds available in the recipient’s account within ten seconds. The EPC notes that SCT Inst rules require participants to process and settle transactions within nine seconds, and the service operates 24/7/365.

- SEPA Direct Debit (SDD). A payment initiated by the payee based on the payer’s consent via a direct debit mandate. This allows utility providers or subscription services to pull funds from your account automatically.

All three instruments rely on the International Bank Account Number (IBAN) as the standard identifier for payment accounts. When you open a euro payment account with a bank or credit union in the EU, you receive an IBAN—a unique combination of numbers and letters that identifies your account within SEPA. An IBAN starts with a two‑letter country code (IE for Ireland, DE for Germany), followed by two check digits and a country‑specific account number. Although IBAN lengths differ, they can be up to 34 characters long. IBANs allow your bank to process cross‑border payments automatically and reduce errors. They became mandatory identifiers for all SEPA accounts in 2014.

Contrasts and Trade‑Offs: Cost, Speed and Reach

Understanding how SEPA transfers differ from traditional wire transfers or domestic bank transfers requires looking at the trade‑offs between cost, speed and geographic coverage.

Cost and Fee Parity

One of the most striking benefits of SEPA is cost parity. Euro transfers within SEPA must be as affordable as domestic transfers. The Central Bank of Ireland explains that cross‑border euro bank transfers within SEPA can be made “just as quickly, easily and cheaply” as payments within your home country. This is because EU legislation prohibits payment service providers from charging more for cross‑border euro payments than they would for equivalent domestic euro payments within the same country. This rule applies to both credit transfers and direct debits. It means, for example, that paying a supplier in France from a German bank account should not incur higher fees than paying a supplier within Germany.

The arrival of instant payments has introduced a new dimension. Regulation (EU) 2024/886—the Instant Payments Regulation—requires payment service providers that offer standard credit transfers to also offer instant credit transfers. It further mandates that any charges levied for sending and receiving instant credit transfers must not be higher than the charges for regular credit transfers of the same type. In other words, banks cannot penalise customers for choosing immediate transfers over standard ones. Still, providers may set their own transaction limits, and some banks may not yet have adopted SCT Inst widely. For large‑value payments, banks may still require traditional wire transfers, particularly when currencies other than euros are involved.

Speed and Availability

Speed differentiates SEPA credit transfers from instant transfers. A standard SEPA credit transfer is typically settled by the next business day, similar to ACH payments in the US. SEPA Instant Credit Transfer, by contrast, requires that funds be available in the recipient’s account within ten seconds. The EPC’s rulebook sets a processing time limit of nine seconds for participants and emphasises that the service is available around the clock. This constant availability is a significant upgrade over traditional bank transfers, which might be delayed over weekends or holidays.

However, not all banks and payment service providers currently offer SEPA instant payments. Adoption has been gradual: some countries have reached majority coverage, while others still lack participants. The new regulation sets staggered deadlines for eurozone and non‑eurozone Member States to implement sending and receiving instant payments by 2025 and 2027, respectively. As more providers join the system, instant transfers will likely become the default for euro payments, but until then, users must confirm whether their bank supports SCT Inst.

Geographic Coverage and Currency Scope

SEPA covers 41 countries, making it broader than the eurozone and even the European Union. This means that customers in countries like Switzerland, Norway or the United Kingdom (where banks still offer euro accounts) can send and receive euro payments through SEPA. Yet SEPA is euro‑only. If you need to transfer other currencies—pounds, dollars or zlotys—you will fall back on other networks, often involving SWIFT messages and currency conversion. Within the EU/EEA, the principle of fee parity applies only to euro-denominated transactions; it does not extend to payments in other currencies.

Cross‑Border Convenience: IBAN Uniformity and Non‑Discrimination

The standardisation of IBANs ensures that you can use a single payment account for all euro transfers in SEPA. A French freelancer working in Ireland, for example, can receive their salary in a French account without needing a local bank. Similarly, an Irish consumer can pay a utility provider in Spain using their Irish IBAN. Article 9 of the SEPA Regulation prohibits IBAN discrimination: businesses and employers cannot refuse to accept your SEPA IBAN simply because it is issued in another country. This means you do not need to open multiple accounts across Europe to handle euro payments.

Trade‑offs exist, though. While one IBAN suffices for euro payments, you may still need a multi‑currency account if your income or expenses involve other currencies. The practice of maintaining balances in euros and other currencies can reduce conversion costs and help you manage currency risk. Our supporting article How to Manage Multiple Currencies in One Account explores these strategies and the trade-offs of holding multiple balances.

Connecting SEPA to the Broader Payment Landscape

Understanding SEPA transfers explained is only part of the picture. To see where SEPA fits within the global payment system, it helps to compare it with other mechanisms and consider what happens when payments leave the euro area.

SEPA vs ACH and SWIFT

SEPA is often called Europe’s version of ACH, but the analogy goes only so far. ACH payments in the US facilitate domestic transfers in dollars; SEPA facilitates domestic and cross‑border transfers in euros. ACH rarely handles high‑value payments or international remittances; for those, US banks use wire transfers routed through Fedwire or the Clearing House Interbank Payments System. SEPA, by contrast, eliminates the distinction between domestic and cross‑border euro transfers within its region. When euro payments cross continents, however, banks typically rely on the SWIFT messaging network to exchange information and settle through correspondent banks. To learn more about how international wires work and how SWIFT supports global payments, see our supporting article What Is SWIFT and How Do International Wires Work?

SEPA and International Fees

SEPA’s fee parity rule applies only to euro payments within the EU/EEA. If you send euros outside SEPA—to the United States or Asia—banks will likely charge higher fees and mark up the exchange rate. Even within SEPA, currency conversion may be required if you hold funds in pounds or dollars. Our supporting article, International Money Transfer Fees Explained, delves into how banks set transfer fees and exchange margins and how to calculate the real cost of a cross‑currency transfer. For consumers and freelancers, understanding these fees is key to choosing the right payment method.

SEPA Delays and Compliance Checks

While SEPA credit transfers usually settle within one business day, delays can occur. Compliance checks, cut‑off times and weekends may affect processing. SEPA instant payments solve this by operating around the clock, but they are subject to daily processing limits and adoption barriers. Our supporting article Why International Transfers Get Delayed explores common reasons for payment delays—including anti‑money‑laundering checks, incomplete recipient details and bank holidays—and offers guidance on setting realistic expectations when sending money across borders.

Clarity on SEPA

SEPA transfers unify Europe’s fragmented bank payment systems, delivering a domestic‑like experience for euro transfers across 41 countries. Thanks to harmonised standards, a French, German or Irish IBAN functions like a domestic account wherever you go. You can pay a landlord in Spain, receive wages from Germany and set up utilities in Italy without opening new bank accounts. The introduction of SEPA instant payments promises near‑immediate settlement, meeting the expectations of an increasingly digital and mobile society. Regulation ensures that charges for these instant payments cannot exceed those for standard transfers, preserving affordability even as the technology improves.

Still, trade‑offs remain. While SEPA simplifies euro transactions, it is euro‑only; sending pounds, kroner, or dollars still involves currency conversion and separate networks. Not all banks participate in SEPA instant payments yet, and large payments or those crossing into other currencies may require SWIFT. Understanding these limitations helps set realistic expectations and choose the right payment method. In the broader context of global payments, SEPA sits alongside ACH, SWIFT and emerging instant payment networks.

If you want to explore how SEPA fits into the wider ecosystem of payment systems and international money transfers, our article on Payment Systems & International Money Transfers provides a comprehensive overview. It connects SEPA to other domestic and global networks, explaining how money moves between banks, across borders and through digital wallets.

Knowing the Euro Pathways

Taking a step back, the idea of SEPA may have seemed daunting—an acronym hidden in financial paperwork, a system that only banks understood. Now, with SEPA transfers explained, the landscape should feel clearer. SEPA is the European infrastructure that makes euro transfers feel local even when the payer and payee live in different countries. It relies on standardised IBANs, ensures fee parity, offers both next‑day and instant transfer options, and operates within a defined currency boundary. By understanding SEPA’s functions and limitations, you can navigate euro payments with confidence, whether paying rent abroad, receiving wages from another country, or managing multiple currencies. The next time someone mentions SEPA, you’ll know it’s not just another acronym but a cornerstone of a unified European payment experience.