How Money Moves — What Happens After You Spend Money

Money doesn’t vanish when you hand it over. It travels, changing hands and purposes, connecting people, businesses, banks, and governments. Yet many people use money daily without thinking about where it goes next. From what I’ve seen, confusion about “money flow” often comes from imagining money sits somewhere after it’s spent. The truth is more interesting: money is designed to move. This article explains why money keeps circulating, how that flow sustains economic life, and why hoarding can slow everything down. We’ll avoid jargon and charts; instead, we’ll use everyday examples and a calm, cause-and-effect story.

Table of Contents

Why Money Needs to Move

Picture money as water running through a city. If water stopped moving, taps would run dry, and plants would wither. Similarly, money moving from person to person and business to business keeps commerce alive. Economists sometimes use a “circular flow” model to illustrate this. It shows money moving endlessly from producers to households and back again. In the simplest version, businesses pay households wages for work, and households use those wages to buy goods and services. The same dollars flow back and forth, allowing goods to be produced and consumed. A healthy economy depends on this continuous exchange; when money stops circulating, activity slows down, just as stagnant water breeds problems. The model also teaches that no single sector should hoard all resources; funds tend to flow continuously between sectors, so each can operate properly.

Money’s movement isn’t random. It’s guided by needs and choices. When you receive a paycheck, that money doesn’t stay in your wallet forever. You pay for groceries, rent, and utilities. The grocery store uses your payment to restock shelves and pay its employees. Those employees, in turn, spend their wages on their own needs. Even if you save part of your paycheck, the money rarely sits idle. Banks lend a portion of deposits to businesses and consumers, so your savings eventually re-enter the cycle as someone else’s spending. Every dollar is a traveller, constantly moving to buy goods, pay wages, or settle debts.

How People, Businesses, and Wages Interconnect

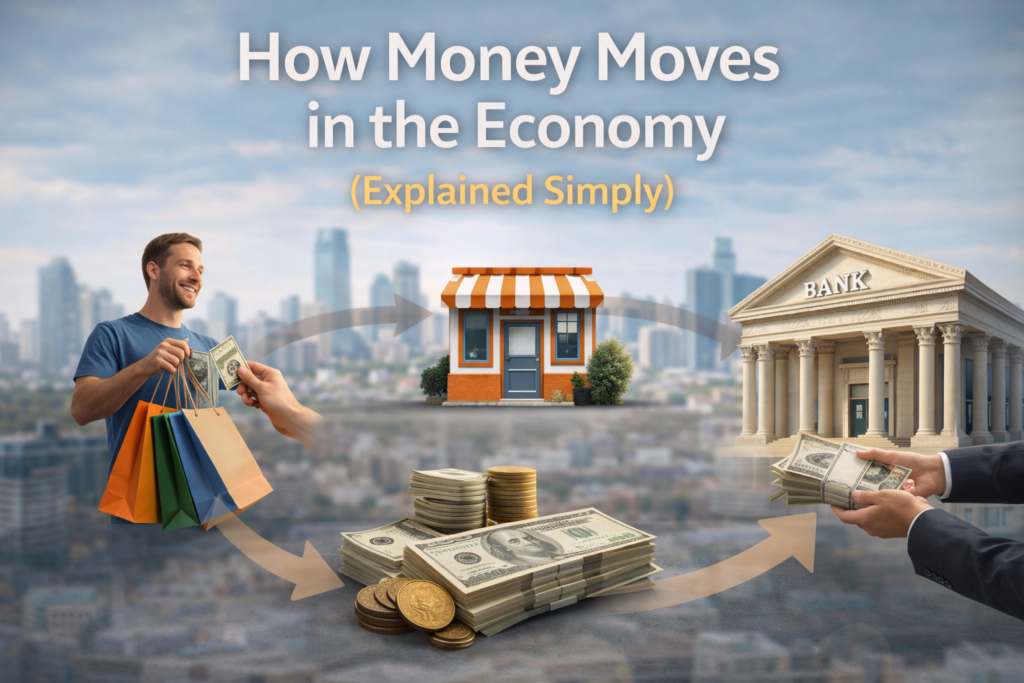

Think about your local coffee shop. You hand over $5 for a cup of coffee. That $5 flows through several hands. First, it becomes revenue for the shop, which uses it to pay baristas’ wages, rent, and utility bills. The shop also orders coffee beans and milk from suppliers, sending some of your money to farmers and dairies. The barista uses part of their wages to buy groceries, pay rent, or pay down a student loan. The landlord uses rent payments to maintain the property and pay their mortgage. The grocery store uses receipts to stock goods and pay staff. Each transaction pushes the money along. It doesn’t stop until someone decides to hold it, but even then, the bank uses it to make loans, so the flow continues.

Now imagine wages. Businesses pay employees for their work. Those wages circulate when employees buy goods and services. The circular flow model highlights that wages from businesses flow to households and back to producers as payment for products. It’s a constant exchange: labour creates value, value earns wages, and wages buy goods. The cycle repeats. If wages rise across the economy, households have more money to spend, increasing business revenue. Conversely, if wages stagnate or unemployment rises, households spend less, and businesses see less revenue. The flow of money through wages is therefore a key driver of economic health.

Why Money Doesn’t Disappear When It’s Spent

One common misconception is that money “disappears” after spending. In reality, spending simply transfers money to another person or organisation. When you pay your internet bill, the money goes to the telecom company. The company uses it to pay technicians, buy equipment, and service its debt. The technicians then pay their own bills and purchase goods. The money you spent keeps moving. If you pay a government tax, the government uses those funds to build roads, pay teachers, and run public services. Those workers then spend their income, and the cycle continues.

This concept applies even at large scales. Government spending and taxation are major arteries of money flow. Taxes take money out of the private sector, but government spending puts money back in by paying salaries, buying goods, and funding projects. A balance between inflow and outflow ensures that money keeps circulating. If taxes are collected but not spent, money would be removed from the economy, reducing the flow. Similarly, if the government spends too much relative to taxes, it injects more money into the cycle, influencing prices and overall activity.

Banks: Connecting Savers and Borrowers

Banks play a special role in the flow of money because they act as connectors. Most money today exists as numbers in bank accounts rather than physical notes. When you deposit money in a checking account, the bank doesn’t keep it in a vault waiting for you. Instead, banks hold only a fraction of deposits as reserves and lend the rest to borrowers. An educational macroeconomics resource notes that “most money is in the form of bank accounts” and that “the banking system can literally create money through the process of making loans”. When a bank lends to a business or individual, it credits their account, increasing the amount of money in circulation. As long as the loan recipient uses the funds and someone else deposits them, the cycle continues.

Consider a simple example: you deposit $1,000 in your savings account. The bank may keep $100 as required reserves and lend $900 to a local restaurant that needs to buy new equipment. The restaurant pays a supplier, who deposits the money into their own bank. That bank can then lend most of it out again. Through this process, known as fractional reserve banking, banks support business activity and help money circulate more widely. The macroeconomics resource explains that a bank must hold enough reserves to meet withdrawals, but the rest can be loaned out, and those loans, when deposited, add to the money supply. In this way, money isn’t sitting still in bank vaults; it’s constantly working as loans, earning interest for the bank and providing funds for businesses and consumers.

How Saving Fits Into the Flow

Saving seems like the opposite of spending, but it still contributes to money circulation. When individuals save money, they usually deposit it in a bank or invest it in financial products. Banks lend these savings to borrowers. A portion of savings may also go into mutual funds, bonds, or other investments, which finance companies and governments. The money thus flows through financial markets. Even money kept in a savings account is not idle; banks use it to fund mortgages, car loans, and business expansions. So saving doesn’t remove money from circulation; it redirects it through financial channels.

It’s important to recognise that excessive hoarding — keeping large amounts of cash at home or under a mattress — slows the flow. When money sits unused, businesses have less access to funds for expansion, and households have fewer wages to earn. On the other hand, prudent saving allows individuals to build security while still letting money circulate via banks and investments. The key is balance: money should move enough to keep goods and services flowing, but households should still build reserves for emergencies and goals.

Spending, Borrowing, and Investing: Different Paths for Money

Money moves in different ways depending on what people and businesses do with it. Spending moves money directly into the hands of businesses and workers, driving demand for goods and services. Borrowing moves money into the hands of borrowers, who spend it on big purchases like homes or equipment. Investing moves money into financial assets, which fund companies and governments. Each path keeps the flow going.

When a family takes out a mortgage to buy a home, they don’t hand over a stack of cash. The bank creates a deposit in the seller’s account and records a loan on the buyer’s account. The seller uses the funds to buy another home, pay down debts, or invest. The buyer repays the loan over time, and the bank uses those payments to make new loans. Similarly, when a business issues bonds or stock, investors provide money that the company uses for research, new facilities, or hiring. In each case, money flows from savers to borrowers, funding productive activities and generating new wages and spending.

Government and Public Spending

Governments collect taxes and borrow money through bonds to finance public services. The money governments spend becomes income for teachers, firefighters, construction workers, and countless other public employees. They, in turn, spend their salaries on goods and services, continuing the cycle. Governments also purchase goods and services directly, such as building roads, buying medical equipment, or contracting software development. These payments go to private companies, which use the funds to pay workers and suppliers. Thus, government spending channels money into the economy just as consumer and business spending do.

Taxes, on the other hand, remove money from the private sector. But taxes are not a one‑way street; they fund the services and infrastructure that support economic activity. Roads, schools, and public safety enable businesses to operate and people to work and spend. In this way, even taxes are part of the flow: they allow the government to circulate money in areas that may not be profitable for private enterprises but are vital for society.

Why Circulation Matters More Than Hoarding

Money is most useful when it is exchanged for goods and services. Imagine everyone decided to hold onto all their cash without spending it. Businesses would see sales plummet, leading them to cut jobs or close. People who depend on wages would have less or no income, leading to more hoarding. It’s a vicious cycle. By contrast, when money flows smoothly, businesses can sell products, pay wages, and invest in growth; workers earn wages and spend them; and the government can tax and spend to provide public goods. The Investopedia article on the circular flow model emphasises that the model shows money moving between producers and consumers and that funds flow continuously between sectors. It also notes that no single sector should collect all resources because the circular flow relies on continuous movement. This continuous movement is what keeps the economy functioning.

It’s natural to be cautious and save for the future. Saving is part of the circulation because banks and financial markets use those funds to finance new projects. The problem arises when money is hoarded outside the financial system, such as cash hidden away. In that case, the money is effectively removed from circulation, reducing the funds available for lending and spending. Some degree of hoarding occurs when people lose trust in the banking system or expect prices to fall (deflation), but in normal times, keeping money moving is better for everyone.

Linking Back to the Bigger Picture

Understanding how money moves helps demystify the broader economy. It builds on earlier lessons about what money is and where it comes from. Remember that money is a shared agreement, not a magical substance. It gained its forms — from shells to coins to digital balances — because people needed an easier way to trade. Our Money Basics: What Money Is, How It Works, and Why It Matters guide explains that money exists as a medium of exchange, a unit of account, and a store of value. This article expands on that by showing that money’s role as a medium of exchange depends on movement. If money stops moving, it can’t perform that role.

For those curious about where money originated, A Brief History of Money (From Barter to Digital) shows how money forms evolved to solve problems like portability and trust. Understanding that history makes it easier to appreciate why banks and digital payments exist today. Similarly, knowing how money flows lays the groundwork for understanding inflation. When too much money chases the same amount of goods, prices rise. Our Inflation 101: Why Prices Go Up Over Time article explains how price changes relate to money supply and demand.

Final Thoughts: Seeing the Flow in Everyday Life

From what I’ve seen, seeing money as part of a flow rather than a static object changes how you think about earning and spending. When you shop at a local market, your dollars support the shop owner, their employees, and their suppliers. When you pay taxes, you fund public services that keep society running. When you save at a bank, your money becomes someone else’s mortgage or business loan. Money doesn’t disappear; it travels, linking countless people and organisations.

Understanding this flow can also make economic news less intimidating. Headlines about interest rates, government spending, or consumer confidence are all about how quickly money is moving. If the flow slows — because people are fearful, banks are cautious, or governments cut spending — economies can stall. If money flows too quickly, prices can rise too fast. Policymakers adjust taxes, spending, and interest rates to try to keep the flow steady.

At a personal level, knowing that money is meant to move encourages balanced habits. Spend wisely on things that matter to you and support your community. Save enough to feel secure, knowing that your savings will still circulate via banks and investments. Avoid hoarding cash out of fear. When money flows, opportunities grow. The economy is not a mysterious machine; it’s a network of human transactions, and money is the lifeblood that keeps it alive.